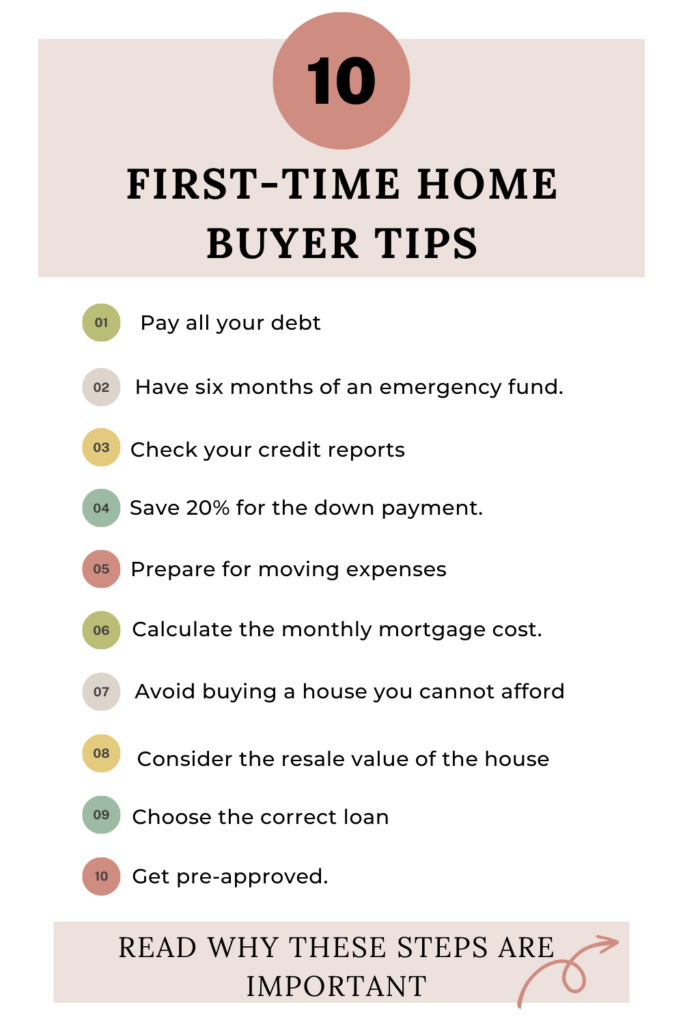

A house is one of the most expensive purchases of our life, so we must be cautious about it. If you make a mistake when purchasing your home, it can be costly and stressful to fix. As a first-time home buyer, try to be as informed as possible about the process and how to prepare for this big step. Here are ten tips to help you plan for this purchase.

Tip#1: Pay all your debt

Most financial experts recommend you pay all your debt before you purchase a house. This will allow you to have a solid foundation. In many cases, buying a house when you are still in debt can turn your dream into a nightmare because debt weighs down your income. As a first-time home buyer, you may not be familiar with all the expenses of owning a home, but you must be prepared for that. Therefore, get rid of all your debt. After all, having a mortgage plus debts equals stress and a higher risk of foreclosure, and you don’t want that!

Moreover, debt can increase your debt-to-income ratio (DTI). The debt-to-income ratio is important because this may determine if you qualify for a mortgage, the amount you qualify for, and the interest rate you will get. Lenders will ask you for your bank statements, and they will pay close attention to the debt you have. They calculate your ratio by dividing all your monthly debt payments by your gross monthly income. This number helps your lender determine your ability to manage the monthly payments to repay the money you plan to borrow. According to the consumer financial protection bureau, “The 43 percent debt-to-income ratio is important because, in most cases, that is the highest ratio a borrower can have and still get a qualified Mortgage.”

This is how you calculate your ratio

- Add up all your monthly debt payments

- Divide them by your gross monthly income. (Your gross monthly income is generally the money you have earned before your taxes and other deductions are taken out.)

Here is one example

Mark has a gross income (before taxes and other deductions) of $5,000 a month. He pays $200 a month for a car loan, $1200 for rent, and $300 for a personal loan. Mark will add up 200+1200+300=$1,700. Then, he will divide the total of his debt by his income (1700 ÷ 5,000=34%). As a result Mark ratio is 34%.

Tip#2: Have six months of saved emergency funds.

This will allow you to be protected in case something unexpected happens. You have to be proactive and prepare ahead for difficult times. Bad things will happen; it is just a matter of time. Remember, emergency funds should only be used for emergencies, and when you take a certain amount, try to put it back as soon as possible. As a first-time home buyer, having the emergency fund in place is the difference between a situation becoming a headache or an inconvenience.

Tip#3 Check your credit reports and credit scores

Way before you begin the home-buying process, you should check your credit reports to get an idea of what you can afford. Your credit scores can significantly affect how much money you can borrow from the mortgage lender and the interest rate you may pay. Also, knowing the details of your credit report allows you to take any action needed to improve your score. Every 12 months, you are entitled to a free copy of your credit reports from all three nationwide credit bureaus.

Tip#4: Save 20% for the down payment.

This will prevent you from paying thousands of dollars for private mortgage insurance (PMI). As a first-time home buyer, you don’t want this extra cost. PMI insurance can cost you from 0.55% to 2.25% of the original loan. The worst part is that this insurance doesn’t protect you; it protects your lender. You don’t want to have this additional cost tearing down your budget. I know that saving the 20% down payment can seem challenging and distant, but if you are intentional about it, you can do it. As mentioned before, having a solid foundation will give you tranquility and allow you and your family to enjoy the process of owning a house much more.

Tip#5 Prepare for moving expenses

You don’t want to be one of those people who borrow money to cover the closing and moving expenses because they did not prepare for it. The average cost for moving less than 100 miles is between $650 to $1800. Prepare for this cost so it doesn’t get you by surprise.

Tip#6: Calculate how much your mortgage will cost you

A written plan is always the key to success in everything you do; this is no exception when buying a house. Calculate your mortgage cost. Include the principal, property taxes, interest, and homeowner insurance costs. Some people, depending on their unique situation, will add more costs. Such as private mortgage insurance (PMI) and homeowners association insurance fees (HOA). Once you have the mortgage total, calculate how much the 25% of your take-home income is. Then, make sure your mortgage does not exceed that amount.

Tip#7: Avoid buying a house you cannot afford

As a first-time home buyer, you should not exceed the money you planned to spend on the house. Many people make this mistake. They plan to spend a certain amount on their house, but on the day of the purchase, they choose a house that exceeds that amount. You must stick to your plan when purchasing a house to avoid surprises. Buying a house is a big deal, and you must be proactive when making such an important decision. You want to be in a position to enjoy your house and be able to reach other goals without stressing over your mortgage.

Tip#8 Consider the resale value of the house

Sometimes we think we have purchased the house of our dreams and won’t even consider the possibility of one day selling the house. However, life constantly changes, and you want to consider this possibility. Perhaps, your family has grown, or there has been a change in your job. There are many reasons why we could end up moving from our home. Therefore, when buying a house, think about the location of the house you like, the structure, and the features. This will be significantly important if you decide to sell it.

TIP# 9 Choose the correct loan

Most financial experts recommend the 15 years fixed rate conventional loan. The reason is that a fixed-rate loan sets the seal on your interest rate for the life of the loan. This means that your lender cannot change the interest rate of your loan in the future.

Moreover, this loan will save you thousands of dollars since you will spend less time paying interest. The difference between a 15 years loan and a 30 years loan could be hundreds of thousands of dollars. Although the 15 years loan has a higher monthly payment, more money goes toward the principal. Therefore, you are paying more toward your debt and less toward interest. Below are the other types of loans available. Also, remember that first-time home buyer loans and grants vary from state to state.

30 years mortgage

The interest rate is too high, and the term of your debt span decades. Also, you end up paying tens of thousands (if not hundreds of thousands) more on interest and other fees than the 15 years loan.

FHA loan (Federal Housing Administration)

This loan will allow you to buy a house with a low down payment. However, like the 30 years loan, this will cost you hundreds of thousands of dollars. With this loan, you can buy a house with as little as a 3.5% down payment. In return, you must pay extra fees for mortgage insurance premium MIP (1.75%). Also, you will have to pay an annual premium (0.85%); this will last for the term of your loan. This is in addition to the fact that you will be paying this loan for 30 years. Try to stay away from this bad deal.

ARM loan

The interest rate can fluctuate. This mortgage usually offers you a lower interest rate at the introductory period of your loan, but the rate will likely increase significantly down the road. As a result, you end up with a much higher monthly payment for your home. Trust me; you don’t want this uncertainty in your life.

VA loans (U.S Department of Veterans Affairs)

This loan doesn’t require a down payment but comes with a funding fee. Also, you don’t want to buy a house with zero down payment. This is because if the market changes, you could own more than the house’s market value. In my opinion, you should never buy a house with zero down payment for many reasons. If you don’t have the money to pay for a downpayment, this is an indicator that you are not ready to purchase a house. Try to avoid any loan that doesn’t require a down payment. The interest on those loans will make your house purchase a terrible deal.

Tip#10 Get pre-approved.

Being pre-approved will give you an advantage over other buyers. It will let the seller know you are ready to make the deal. Finding the ideal home can sometimes be challenging. Therefore, you want to ensure that no one will take it away when you find the house of your dreams.