What is a good credit score?

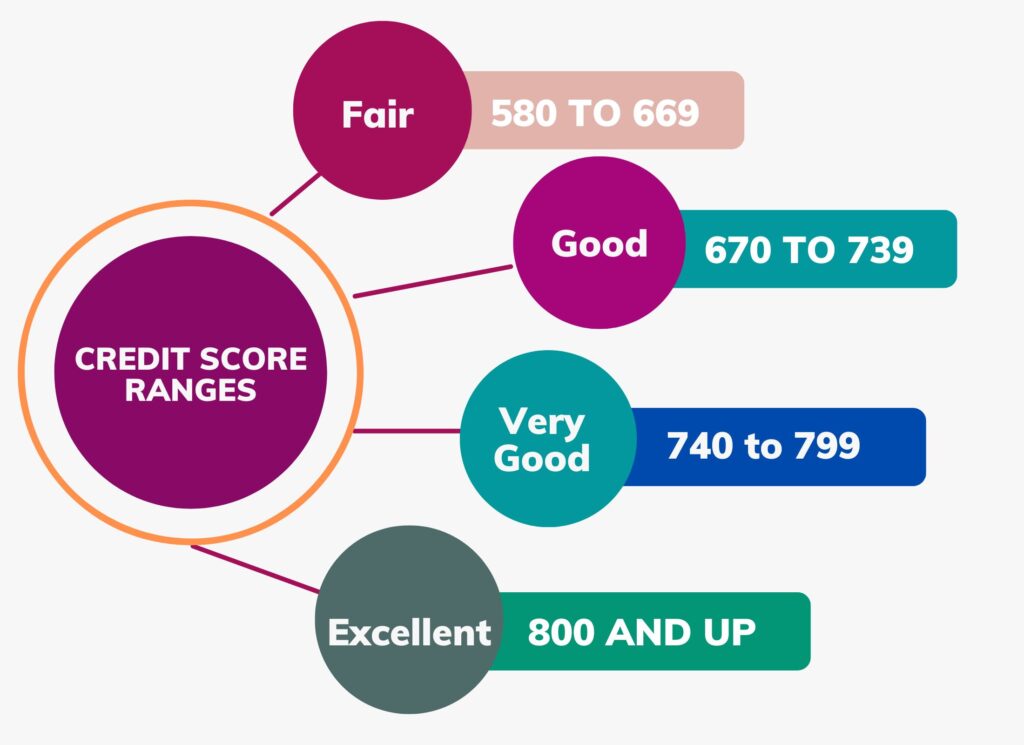

A good credit score is between 670 to 739. However, nobody is born with it, so at some point, we have to start to create one. You probably already know how essential your credit score is when getting a loan, renting an apartment, etc. Here, I will show you how to build your credit history from scratch and if you already have a credit history, but need to improve it, I will show you a good way to do just that.

Get a secured credit card

This card is designed for people with bad or no credit at all. Basically, when you open the account, you will make a deposit which in most cases is equal to the credit limit you will have. The secured credit card is backed by the deposit you make. For instance, you opened an account with a $600 deposit, so your credit limit will be $600.

The deposit protects the issuer. In a case you don’t pay a bill, they will take the money from your deposit to pay for it. If you make all your payments on time, you will eventually get your deposit back. Use the card responsibly, so you can create a good credit history or improve your current score. If you use this card correctly, you can qualify for an unsecured card -one without a deposit requirement.

Get a secured loan

Like secure cards, credit-builder loans, help you build your credit history. They are not widely advertised and are usually offered by credit unions and community banks.

You won’t have access to the loan money during the repayment process. That is until the loan is paid off in full; this protects the lender. As you probably already guessed, this account not only helps you build your credit but also functions as a saving account.

If you decide to do this, make sure you make all the payments on time because the lender will report them to the credit bureau at least one a month. Reporting your payment to the credit bureau is a way to help you build your credit history as long as you pay on time. On the other hand, if you pay late, it will just hurt your credit score.

Become an authorized credit card user

If one of your family members wants to help you build your credit, he/she can add you as an authorized user on his/her card. In turn, your credit report includes his/her credit history. The best part is that you don’t have to use or possess the card in order to benefit from being an authorized user. If you choose to do this, make sure the primary user has a long history of paying on time and he/she uses the card responsibly. Also, make sure you have an explicit agreement about who is responsible for what. Remember, you don’t want to make this deal with someone who will make you pay a debt that you don’t own.

In order for you to play defense with your credit report, you need to know what can affect it. Here is a list of the most significant factors that impact your credit based on the Fico score.

Payment history (FICO 35%)

Your credit history shows whether you’ve consistently paid your bills and other obligations on time. According to FICO, payment history accounts for 35% of your score. I recommend you set up an automatic payment, so you never miss your due date

Credit utilization (FICO 30%)

Credit card utilization is the amount you use from your credit limit. You don’t want to use a high percentage of your credit limit because that will affect your credit score negatively. Many experts recommend you don’t use more than 30% of your credit limit. If you need to use a higher percentage, I recommend you call your creditor and ask for a credit increase, so you can stay within the 30% credit utilization. However, if you ever exceed the 30% utilization, simply make a large payment at the end of the month. Then, when your creditor reports it to the credit bureaus, the balance is within the 30% recommended.

Credit history (FICO 15%)

The older your accounts the better it is for your credit score. Try to keep your accounts open as long as possible.

A mix of credit accounts (FICO 10%)

It’s best to have a mix of installment accounts. Such as credit cards, retail accounts, installment loans, finance company accounts, and mortgage loans. You don’t need one of each just a reasonable mixture.

Credit Inquiries (FICO 10%)

When you apply for credit, the lender will check your credit report; this will cause soft, or hard credit inquiries. Soft inquiries don’t impact your credit score. However, a hard inquiry can drop your score.

After all, be very mindful of your financial moves, so you can maintain good financial health. This include a good credit score. Remember, in order to create a credit history, you will have to borrow money, so be very careful with that. A secured card and loan are the safest way to build your credit history. Once you create good credit, focus your attention on maintaining a good score. Pay your bills on time, don’t use more than 30% of your credit limit, and avoid hard inquiries unless necessary. Finally, get your free credit report once a year, so you see where you stand.