You should start your retirement planning regardless if you want to retire early or at the traditional retirement age of 62 years old and above. Planning involves knowing the specific amount you’ll need and the action plan to get to that amount.

According to the U.S. Department of Labor, “Only half of Americans have calculated how much they need to save for retirement” Aging is unpreventable, so regardless if you are aiming to retire early or not, you have to prepare.

“The question isn’t at what age I want to retire, it’s at what income.”

George Foreman

Here are 8 ways to prepare for your early or traditional retirement.

Figure out your retirement income.

There are a few questions you should ask yourself when doing your retirement planning. Such as, How much I will need in retirement, how much I have to save monthly to reach that number, how much I need in investment to produce my retirement income, etc. You can use an online retirement calculator to help you with that.

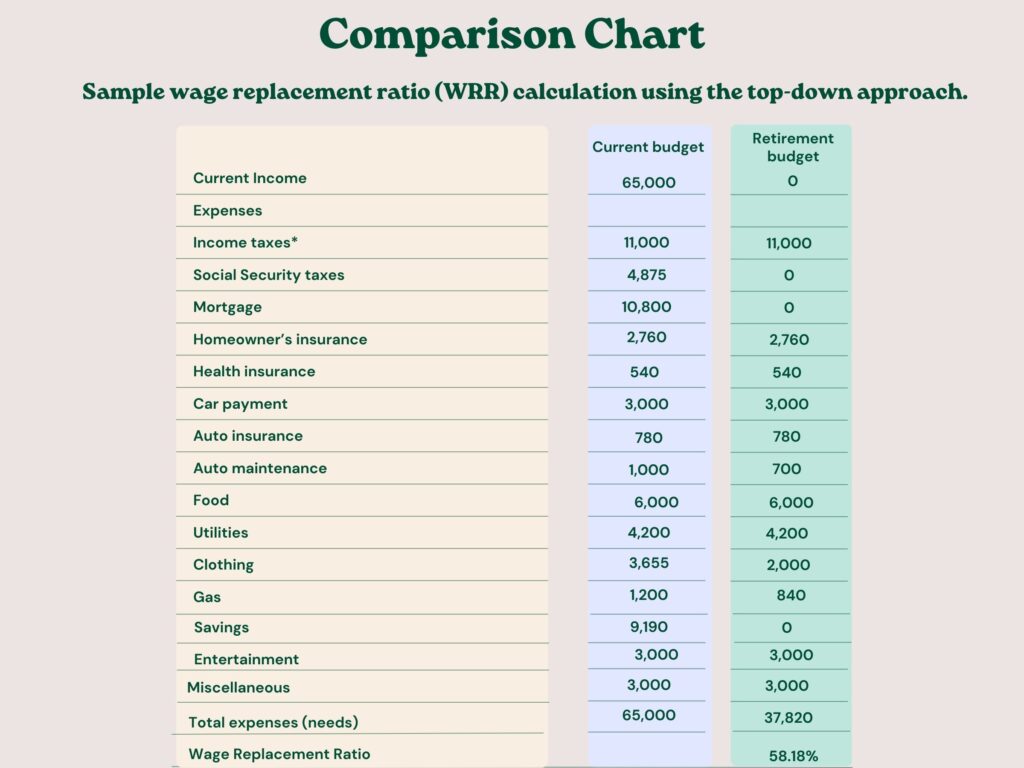

How much you will need in retirement depends on you and your objectives. According to this article by the University of Florida, “On average, many financial planners report that clients need approximately 70%–80% of their pre-retirement income to retire and maintain the same lifestyle (Dalton 2008).”

While this is just an estimate, the specific number depends mainly on your needs. Consider these factors when calculating your retirement number.

- The desired standard of living. Are you planning on keeping the same preretirement lifestyle? Changing your lifestyle could decrease or increase income needs.

- Clothing, food, parking, gas, and other work-related expenses may no longer be needed in retirement.

- Generally, payroll taxes (such as FICA-federal payroll tax) decrease during retirement

- Health-related expenses can potentially increase.

Create an action plan.

Once you have those numbers figured out, you can create an action plan for your retirement. What do you have to do now to reach your retirement goal? Your plan should have a specified amount, date, and step-by-step strategy to reach each goal.

Make saving a priority.

If you are not saving, start today! Remember, the sooner you start saving, the more time your money has to grow. Create a saving plan and stick to it. It will be best if you automate it. In other words, you set a predetermined amount to be transferred from your checking to your saving account on a specific date. This will help you maintain the discipline of consistently saving.

It pays off to save; It provides financial stability. You can start saving a small portion of your paycheck. Then, as you pay off debt or increase your wage, you slowly increase your saving. The most significant advantage of saving is compound interest. For instance, the money you put in a 401K will earn interest or capital gain earnings. As time pass, you also earn interest on your interest or earnings on your earnings. Remember, the earlier you start, the better because you have time.

Invest consistently

Your action plan should include investing because this is the best way to create wealth. Set a monthly transfer from your saving to your brokerage account. Again, automatic transfers help you be consistent. You can also automate your investment on a specific day of the month. This will help you to consistently dollar cost average into the market.

Use tax advantage accounts.

You can use tax advantage accounts to invest for retirements, such as 401Ks and IRAs. These are great vehicles to make the most out of your investment. For instance, Roth IRA accounts allow you to invest after-tax money, so the money grows tax-free.

Similarly, 401k gives you tax advantages. For example, if you invest in your employer-sponsored 401k, you can deduct your contribution from your taxable income. Also, many employers match your contribution up to a certain amount. This is free money; you should take advantage of that if available.

Keep your investment plan simple and consistent.

Unless you are a financial expert, you should avoid complex investments and instead invest in funds that give you instant diversification, like low-cost index funds and ETFs. Actively managed funds and single-stock investing might not be worth your time and money.

According to a CNBC article, “About 80% of all actively managed U.S. stock mutual funds underperformed their benchmark in 2021, the third-worst showing in the past two decades, according to S&P Dow Jones Indices’ annual SPIVA report.”

Check your social security benefit.

As part of your retirement plan, check your social security benefit. This may not apply to those of you who plan to retire early. However, it is still good to know since you will use it eventually.

You can use the Social Security Administration’s website to check your benefit.

Checking your social security benefit is good information, but you should not leave your retirement financial stability to the government. We don’t know if social security will be around when we retire, so don’t count on it too much.

“As far as your personal goals are and what you want to do with your life, it should never have to do with the government. You should never depend on the government for your retirement, your financial security, for anything. If you do, you’re screwed.”

Drew Carey

Create healthy financial habits.

Create a lifestyle that follows your financial goals. If you want to retire wealthy, you must make your priority a priority. It isn’t enough to wish and dream; you have to create healthy financial habits and follow a plan. Here are a few healthy habits to consider.

- Budget; know where each dollar is going.

- Stay out of debt; stop the bleeding and avoid paying high interest.

- Consistently save; keep as much money as possible. Remember, it is not how much money you make but how much you can keep.

- Invest consistently; grow your money by buying assets, such as stock, real estate, and bonds.

- Focus your spending on your needs and less on your wants.

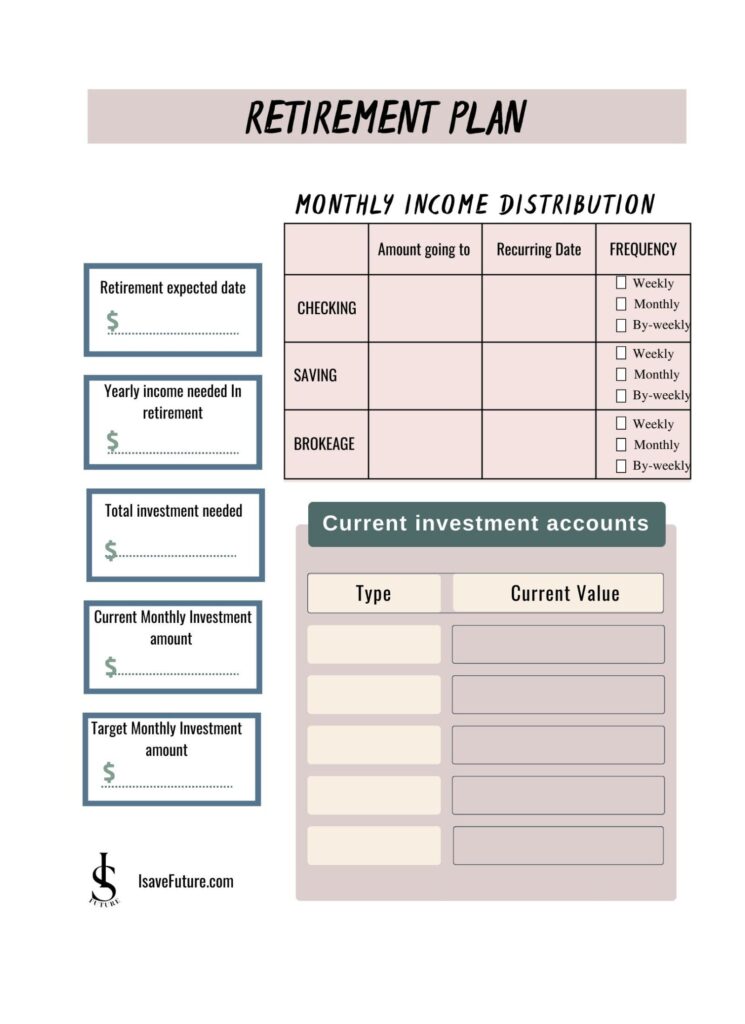

Free Retirement Planning Template