There is a significant difference between term and whole Life Insurance that you should know before deciding on one. Life insurance is recommended for people who are not self-insured. In other words, It is crucial to obtain a policy if you lack sufficient savings/investments to safeguard your loved ones in the event of your unexpected demise. Some experts recommend you have life insurance worth 10 to 12 times your annual income.

Investing information provided in this blog post is solely for educational purposes. Neither IsaveFuture nor its subsidiaries offer advisory or brokerage services, and we do not recommend or advise investors to buy or sell specific stocks, securities, or other investments.

Before navigating this market, you must determine the amount of money you need in your policy, the number of years you will need, and determine what type of insurance is best for you.

What is term life insurance?

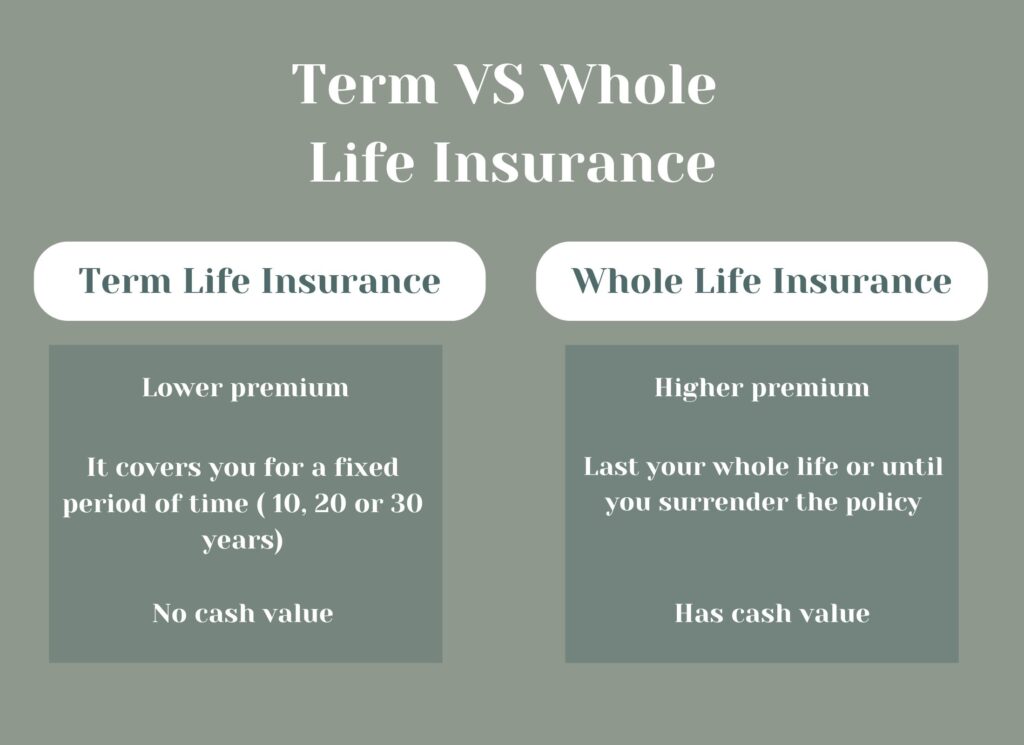

It provides coverage for a specific amount of years, and if you die during the term, it pays your beneficiaries a fixed amount. Paying your beneficiaries is the only function of term life insurance. This is why it is the simplest and more affordable on the market. You can use this Term Life Insurance Calculator to estimate costs.

At the time of purchase, you decide the policy term. Then, the premium will stay the same during the life of the insurance. The most common terms are 10, 20, and 30 years, but other options may be offered. Experts usually recommend a term policy lasting 15-20 years, but it depends on the individual.

How it works

You will buy a term typically 10, 15, 20, or 30 years. During that term, you will make a payment to the insurance company. In return, the insurance company will assume the financial risk of your death during the policy term. If you die during the insurance term, it will pay your beneficiaries the death benefit.

For example, if you purchase a 20 years term life policy with $100,000 in coverage, you are responsible for making monthly payments for those 20 years. If you die during the 20 years term, the insurance company will pay your beneficiaries $100,000. Also known as the death benefit.

What is whole life insurance?

Also known as cash value insurance, whole life insurance lasts as long as you pay the premium. In general, whole-life plans are more expensive than term life for the different functions it serves and their longevity.

This account is designed to accumulate cash value gradually and serves as both an investment and life insurance policy. Financial experts like Dave Ramsey recommend that your investment be separated from your insurance, so they don’t recommend this type of policy. Also, you will most likely not need coverage for your entire life. When you become wealthy and self-insured, you won’t need it.

How it works

The first step is to decide the policy amount (death benefit) you want. This is the amount you want your beneficiaries to get when you die. Based on this amount, you will pay a monthly premium. Your policy will be valid for as long as you pay that premium. From this point forward, the insurance company will divide the money you pay in premiums into two accounts. Part of the money goes into the cash value account. The other part of the premium will cover your policy’s actual life insurance part.

These policies earn interest in a tax-advantaged account and offer guaranteed returns, but they’re expensive and unsuitable for most people.

Factors you should know about whole life insurance.

- Initially, a significant amount of the policyholder’s premiums go towards building the cash value within the policy. However, in the later years, more of your premiums are going toward your policy because the insurance cost will increase as you age.

- The insurance company will keep the money if you don’t use the cash value while alive. Your family will only get the death benefits.

- If the cash value is available and your account has not matured, you can take some money, but it will come at a high price. You can take out a loan against your policy, but you must pay interest even though it is your money. Also, if you don’t repay the borrowed money, the insurance company will deduct that amount from your death benefit.

- Another way to tap into the cash value of your whole life insurance is by doing a “cash surrender or cancelation.” Cash surrender value is money the insurance company pays the policyholder if the person voluntarily terminates before maturity or an insured event occurs.

Many experts, such as Dave Ramsey, Suze Orman, and Clark Howard, recommend term life insurance coverage. They consider that whole life insurance is costly. Also, the rate of return in the investment part is low. Dave Ramsey recommends you separate your life insurance from your investment. Also, according to his advice, it is recommended to have life insurance for the duration it takes to accumulate wealth or until we no longer have dependents. Once we are wealthy or have no dependents, there is no need for it.